As the insurance market reflects on 2025, one conclusion is difficult to avoid: climate-driven losses are no longer episodic or peripheral. They are structural, persistent and increasingly driven by so-called “non-peak” perils. Wildfires, flooding and severe thunderstorms once again defined the claims environment, reshaping loss patterns globally, including the UK and Europe. These conditions that drove losses in 2025 are unlikely to abate in 2026.

2025 in Review: Non-Peak Perils Dominate

From a global perspective, 2025 became the costliest claims year on record for non-peak perils. Wildfires, flooding and severe convective storms accounted for almost all insured catastrophe losses, pushing global insured losses back above US$100 billion. While total economic losses were lower than the ten-year average, largely due to the absence of a major US hurricane landfall, the insurance sector still faced substantial balance-sheet pressure.

The year illustrated a key shift in risk dynamics. The United States avoided a direct hurricane hit for the first time in a decade, yet losses remained elevated. Events such as widespread wildfires and severe thunderstorms proved that insurers can no longer rely on a ‘quiet’ hurricane season to limit annual loss volatility.

Globally, natural catastrophe-related fatalities rose to approximately 17,200 in 2025, significantly higher than in 2024, although still below the long-term average. This reinforces the uneven but intensifying human impact of climate-driven extremes.

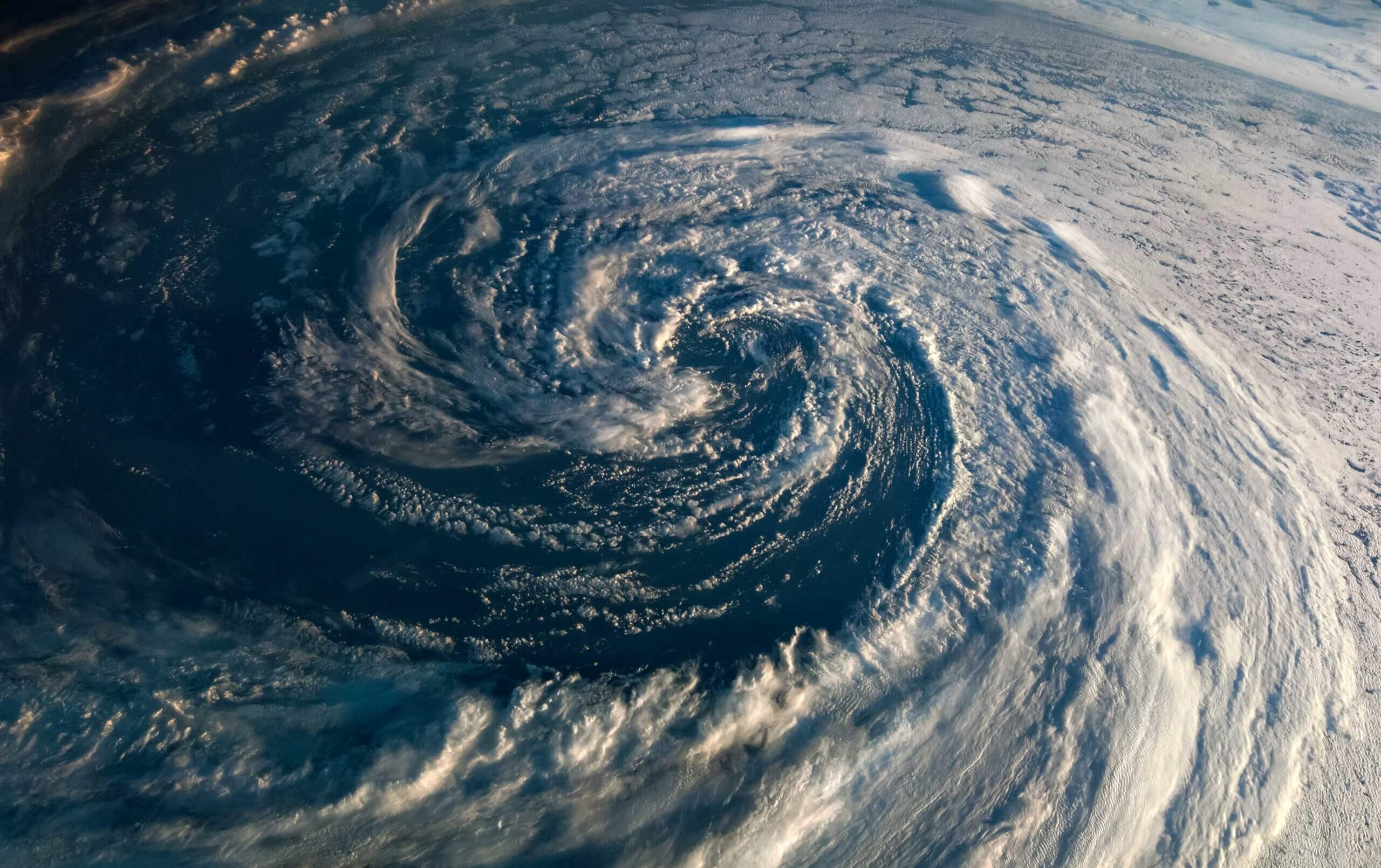

Climate Signals: 2025 Among the Warmest Years on Record

From a climate standpoint, 2025 was one of the warmest years ever recorded. Higher baseline temperatures contributed to prolonged dry periods, intense rainfall and greater atmospheric instability. The result was a rise in wildfires, flash flooding and severe convective storms.

For organisations, this translates into more frequent operational interruption, greater strain on physical assets and increased exposure to events that were previously considered low-probability.

UK Experience: Weather Losses Become the Norm

In the UK, 2025 continued an already worrying trend. Insurers entered the year following record weather-related payouts in 2024, and claims activity remained elevated. Severe storms and flooding in the early part of 2025 resulted in hundreds of millions of pounds in property and business interruption claims, with some quarters setting new records for storm-related losses.

Crucially, many losses occurred outside historically high-risk flood or storm zones. Surface-water flooding, overwhelmed drainage systems, wind damage and power outages affected offices, warehouses, retail premises and professional services firms alike. For many businesses, the primary impact was not physical damage alone, but lost trading time, delayed projects and supply-chain interruption.

Europe: Escalating Economic Losses, Protection Gaps Persist

Across the EU, 2025 reinforced Europe’s exposure to climate volatility. Storms, floods and wildfires generated tens of billions of euros in economic losses, adding to a long-term total that now exceeds €800 billion since 1980. Flooding and storms remained the dominant drivers, but wildfire activity expanded significantly, fuelled by heat and prolonged dry conditions in southern and central Europe.

A persistent challenge across Europe remains the gap between economic losses and insured losses. In many regions, a large proportion of climate-related damage is still uninsured, leaving businesses exposed to unexpected balance-sheet shocks.

What This Means for 2026

Looking ahead, the lessons from 2025 point to several clear expectations for 2026:

- Continued Volatility from Non-Peak Perils Wildfires, severe thunderstorms and flooding are likely to remain primary loss drivers. These events are less predictable, more localised and harder to diversify than traditional peak perils.

- Business interruption exposure deserves renewed focus Losses are increasingly driven by downtime, access issues and supply-chain disruption rather than total property loss.

- Greater Scrutiny of Risk Mitigation Businesses that can demonstrate effective flood resilience, fire mitigation and continuity planning will be better positioned to secure competitive terms. Risk engineering and loss-prevention measures will increasingly influence placement outcomes.

- Growing Importance of Strategic Risk Advice As climate risk becomes more complex and interconnected, the role of informed, forward-looking broking advice will be critical in helping organisations understand their exposures and structure appropriate insurance programmes.

As we move into 2026, businesses that proactively assess climate exposure, strengthen resilience and review their insurance arrangements will be best placed to navigate an increasingly volatile environment.

At W Denis, we work with clients to translate these evolving risks into practical insurance and risk management strategies, helping ensure that climate volatility does not become an avoidable commercial shock. To discuss your insurance options with a broker, contact Daniel Moss at Daniel.moss@Wdenis.co.uk or on 0044 (0) 113 2439812.

Share:

Specialist contact

Mark Dutton

Chief Commercial Officer

T. +44 (0) 7831 366 469

E. mark.dutton@wdenis.co.uk

Arrange a call back